Click to Enlarge

Click to Enlarge At some point prior to accepting an offer on a home listed for sale, the listing agent and seller will request that the buyer provide "evidence of funds" or "proof-of-funds" in an amount greater than or equal to the offered down payment plus closing costs associated with the transaction. This will be in addition to a pre-approval for the loan that the buyer will be utilizing to purchase the home. Of course if the transaction is "all cash" then the seller wants to see evidence of funds for the entire amount of the purchase, plus any anticipated closing costs. Many buyers (especially first time buyers) forget about the closing costs element of the transaction, which can be substantial (about 2.125% of the purchase price, less for all cash buyers). This is certainly understandable, given that most people don't purchase homes on a regular basis -- it's easy to forget between transactions and if you've never purchased a home, you wouldn't know unless someone told you (might be a good topic for a Realtor/buyer conversation!).

Generally buyers will provide (or should provide) a copy of a recent bank statement, brokerage statement, or other documentation that clearly indicates their name, name of the financial institution, at least a partial account number, and the balance in the account. But that's not always the case!

On one occasion, I had a buyer who insisted that they had all cash, but it was just that -- cash! It wasn't in an account anywhere, but he expected home sellers to just "believe" that he had the cash. I suggested that he might put it in an account for a few months to document the funds, or at the very minimum, photo-copy the funds such that a prospective seller could actually see that the cash was real. Needless to say, this particular individual did not wind up buying a home!

The photo above is another example of the "evidence of funds" that I've received. While i don't doubt that these funds exist (or had existed at some point in time), there's no link between these funds and the buyer! It could be a relative, a friend, or anyone for that matter! Evidence such as this won't get your offer accepted and it certainly won't make it past an underwriter.

So the moral of the story is, when you're ready to purchase a home, make certain that your pre-approval is solid (and recent -- and desktop underwriting or "DU" approval is even better) and that you have recent "evidence of funds" in hand!!

Generally buyers will provide (or should provide) a copy of a recent bank statement, brokerage statement, or other documentation that clearly indicates their name, name of the financial institution, at least a partial account number, and the balance in the account. But that's not always the case!

On one occasion, I had a buyer who insisted that they had all cash, but it was just that -- cash! It wasn't in an account anywhere, but he expected home sellers to just "believe" that he had the cash. I suggested that he might put it in an account for a few months to document the funds, or at the very minimum, photo-copy the funds such that a prospective seller could actually see that the cash was real. Needless to say, this particular individual did not wind up buying a home!

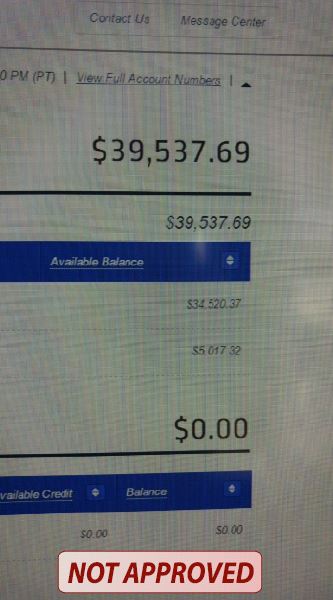

The photo above is another example of the "evidence of funds" that I've received. While i don't doubt that these funds exist (or had existed at some point in time), there's no link between these funds and the buyer! It could be a relative, a friend, or anyone for that matter! Evidence such as this won't get your offer accepted and it certainly won't make it past an underwriter.

So the moral of the story is, when you're ready to purchase a home, make certain that your pre-approval is solid (and recent -- and desktop underwriting or "DU" approval is even better) and that you have recent "evidence of funds" in hand!!

RSS Feed

RSS Feed