After the recent news regarding Wells Fargo's generating fake accounts to meet sales quotas (and the subsequent Senate hearing lambasting the CEO of Wells Fargo) I decided that I couldn't continue, in good conscience, to continue banking with Wells Fargo. In all fairness, Wells Fargo did not (to my knowledge) create any fake accounts on my behalf and has been very efficient over the past many years (although they did abuse one of my sons on many occasions in his young banking life).

But changing banks has not come without some pain (I switched to a local credit union). I use Quicken so that took some effort to get switched over -- it was finally working well, and then I changed the nickname of the account on the credit union side, and that rendered everything inoperable for awhile, so I was back to square one, but it's now working again -- so lesson learned -- don't touch it!

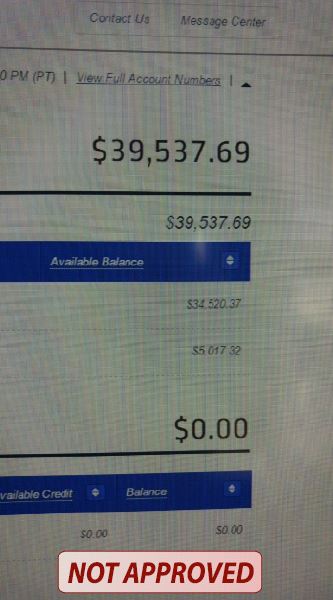

Then I went to make a deposit with my phone -- again, no bueno. Apparently there's a 30-day wait to be able to use mobile banking services. That seems very arbitrary, but then I don't have much of an option so I'll have to wait it out.

So I went to a local ATM, one of many that I can use to make deposits, and that seemed to work well enough. The primary difference (or so I thought at this point) being that they don't email you a receipt -- the ATM prints out a small paper receipt. Again, not the end of the world, but a small step backwards as now there's another piece of paper in my life of which I have to keep track -- and Realtors have plenty of paperwork of which to keep track of already!

The next big difference between Wells Fargo and the credit union is that the CU puts a 4 to 7 day hold on my deposits made by check, and a 3 to 4 day deposit on funds directly transmitted from Wells Fargo (as I slowly drain the account -- there's a monthly limit on how much you can transfer, so it will take a little time to draw down the Wells Fargo account). With Wells Fargo, all deposits were generally available the next business day.

So while I'm committed to the idea, I'm not completely sold on it. Hopefully, once I have a longer term relationship with the credit union they can relax some of their rules, and the transition will have been worth it. So time will tell.

But changing banks has not come without some pain (I switched to a local credit union). I use Quicken so that took some effort to get switched over -- it was finally working well, and then I changed the nickname of the account on the credit union side, and that rendered everything inoperable for awhile, so I was back to square one, but it's now working again -- so lesson learned -- don't touch it!

Then I went to make a deposit with my phone -- again, no bueno. Apparently there's a 30-day wait to be able to use mobile banking services. That seems very arbitrary, but then I don't have much of an option so I'll have to wait it out.

So I went to a local ATM, one of many that I can use to make deposits, and that seemed to work well enough. The primary difference (or so I thought at this point) being that they don't email you a receipt -- the ATM prints out a small paper receipt. Again, not the end of the world, but a small step backwards as now there's another piece of paper in my life of which I have to keep track -- and Realtors have plenty of paperwork of which to keep track of already!

The next big difference between Wells Fargo and the credit union is that the CU puts a 4 to 7 day hold on my deposits made by check, and a 3 to 4 day deposit on funds directly transmitted from Wells Fargo (as I slowly drain the account -- there's a monthly limit on how much you can transfer, so it will take a little time to draw down the Wells Fargo account). With Wells Fargo, all deposits were generally available the next business day.

So while I'm committed to the idea, I'm not completely sold on it. Hopefully, once I have a longer term relationship with the credit union they can relax some of their rules, and the transition will have been worth it. So time will tell.

RSS Feed

RSS Feed